Defending $100,000: Data reveals whether bitcoin will rebound or continue to decline

The market may have entered a mild bear market.

The market may have already entered a mild bear market.

Written by: Chris Beamish, CryptoVizArt, Antoine Colpaert, Glassnode

Translated by: Luffy, Foresight News

Summary

- Bitcoin has fallen below the short-term holder cost basis (around $112,500), confirming weakened demand and officially ending the previous bull phase. The current price is consolidating around $100,000, down about 21% from the all-time high (ATH).

- About 71% of Bitcoin supply remains in profit, consistent with characteristics of a mid-term correction. A relative unrealized loss rate of 3.1% indicates the market is in a mild bear phase rather than a deep capitulation.

- Since July, long-term holder Bitcoin supply has decreased by 300,000 coins, and selling continues even as prices fall—unlike the "sell into strength" pattern seen earlier in this cycle.

- US spot Bitcoin ETFs have seen sustained outflows ($150 million–$700 million daily), and the cumulative volume delta (CVD) on major exchanges shows persistent selling pressure and weakened self-directed trading demand.

- Directional premium in the perpetual futures market has dropped from $338 million per month in April to $118 million, indicating traders are reducing leveraged long positions.

- There is strong demand and rising premiums for put options at the $100,000 strike price, showing traders are still hedging risk rather than buying the dip. Short-term implied volatility remains sensitive to price swings but has stabilized after spiking in October.

- Overall, the market is in a fragile balance: demand is weak, losses are manageable, and caution prevails. A sustained rebound will require renewed capital inflows and reclaiming the $112,000–$113,000 range.

On-chain Insights

Following last week’s report, Bitcoin failed multiple attempts to reclaim the short-term holder cost basis and broke below the psychological $100,000 mark. This breakdown confirms weakened demand momentum and ongoing selling pressure from long-term investors, marking a clear departure from the bull market phase.

This article will assess structural market weakness using on-chain price models and spending indicators, then combine spot, perpetual futures, and options market data to gauge market sentiment and risk positioning for the coming week.

Testing Lower Support Levels

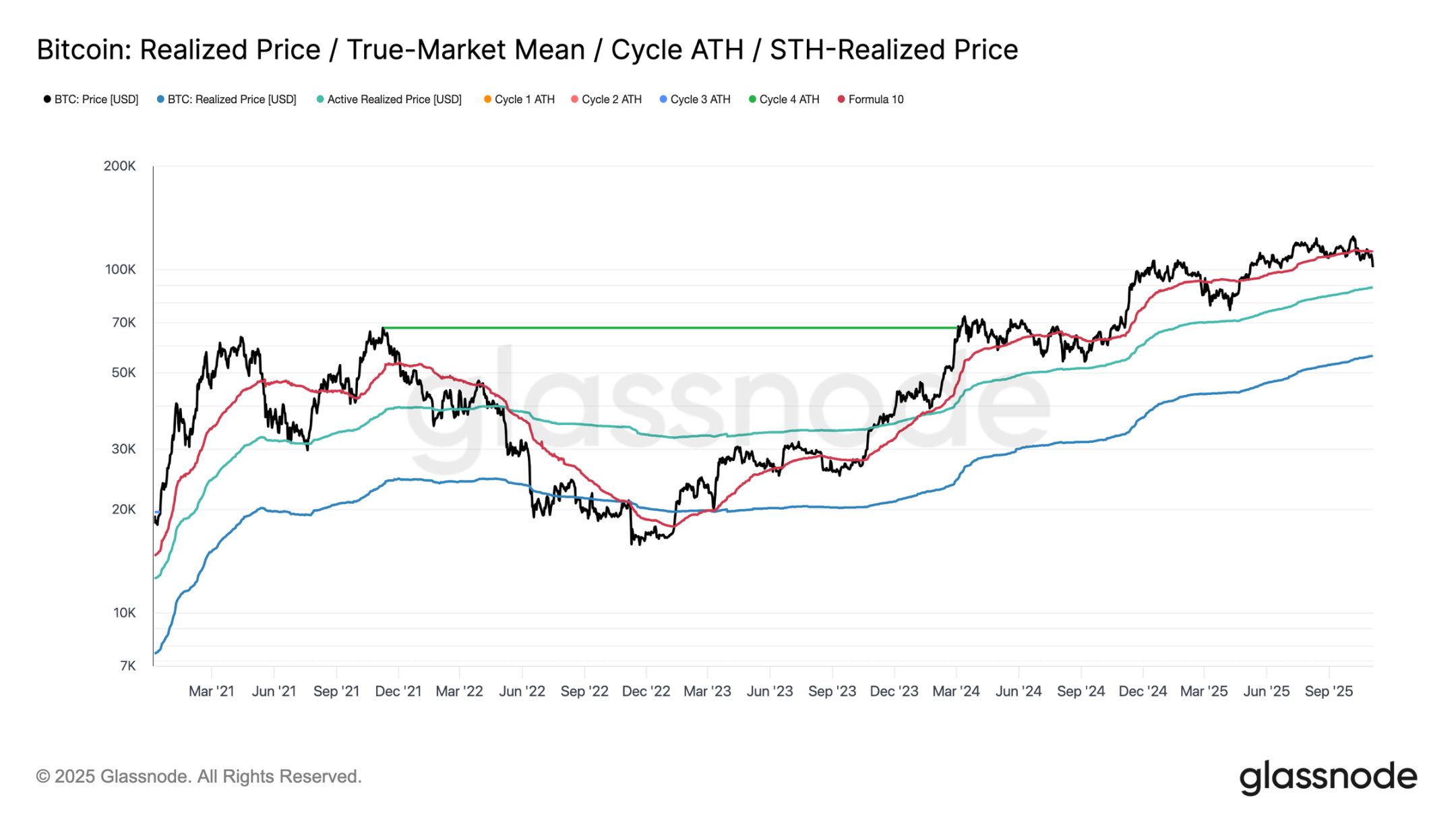

Since the market crash on October 10, Bitcoin has struggled to stay above the short-term holder cost basis, ultimately dropping sharply to around $100,000, about 11% below the key threshold of $112,500.

Historically, when the price trades at such a discount to this level, the likelihood of further declines to lower structural support increases—for example, the realized price of active investors, currently around $88,500. This metric dynamically tracks the cost basis of actively circulating supply (excluding dormant coins) and has served as a key reference during prolonged correction phases in past cycles.

At a Crossroads

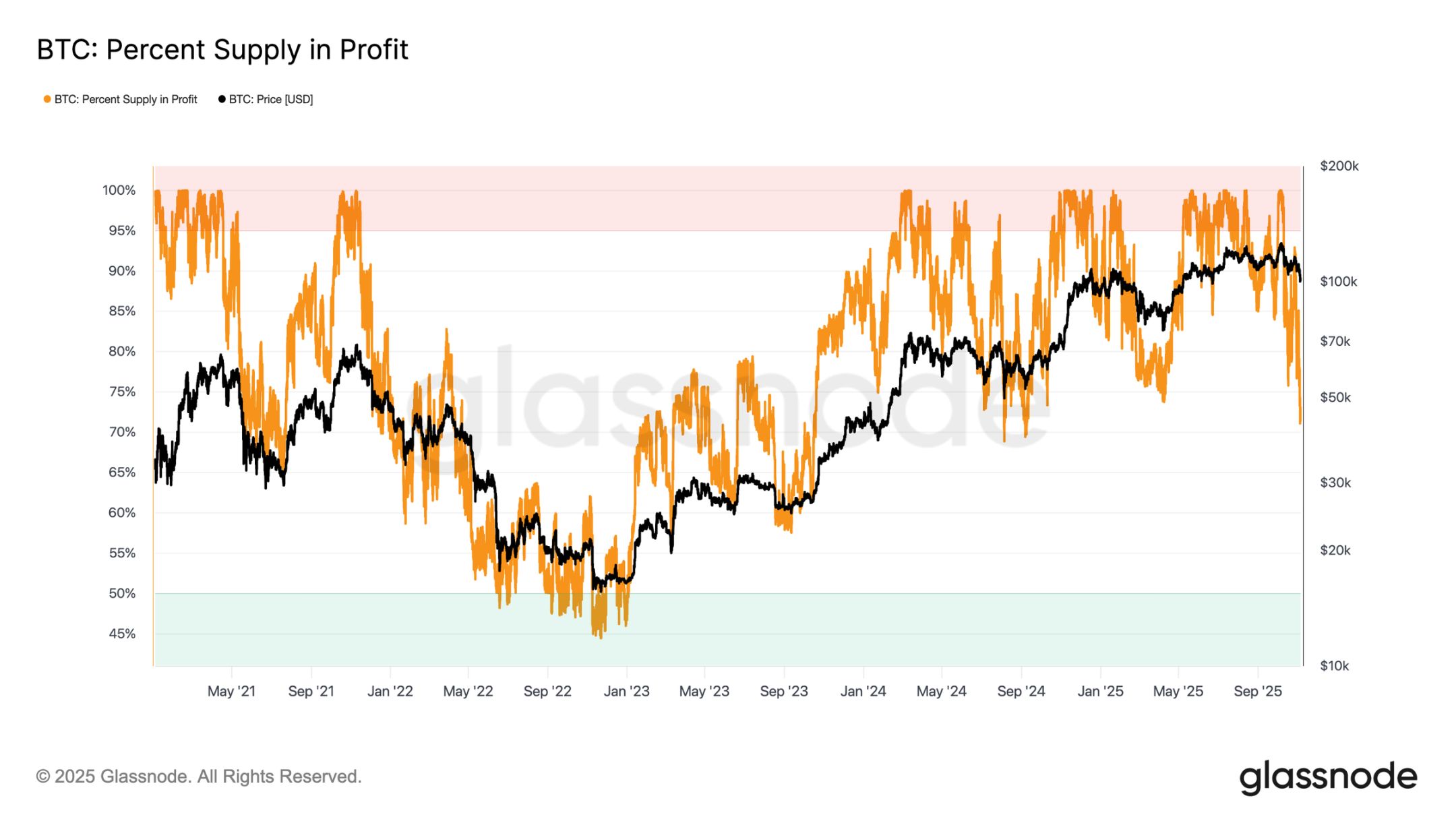

Further analysis reveals that the current correction structure is similar to those in June 2024 and February 2025—periods when Bitcoin was at a critical crossroads between "rebound" and "deep contraction." At the current $100,000 level, about 71% of supply remains in profit, placing the market at the lower end of the typical 70%-90% profit supply equilibrium zone seen in mid-term slowdowns.

This stage often sees brief recoveries toward the short-term holder cost basis, but sustained recovery typically requires prolonged consolidation and new demand inflows. Conversely, if further weakness pushes more holders into loss, the market could transition from the current mild downturn to a deep bear phase. Historically, this stage is characterized by capitulation selling and long-term reaccumulation.

Losses Remain Manageable

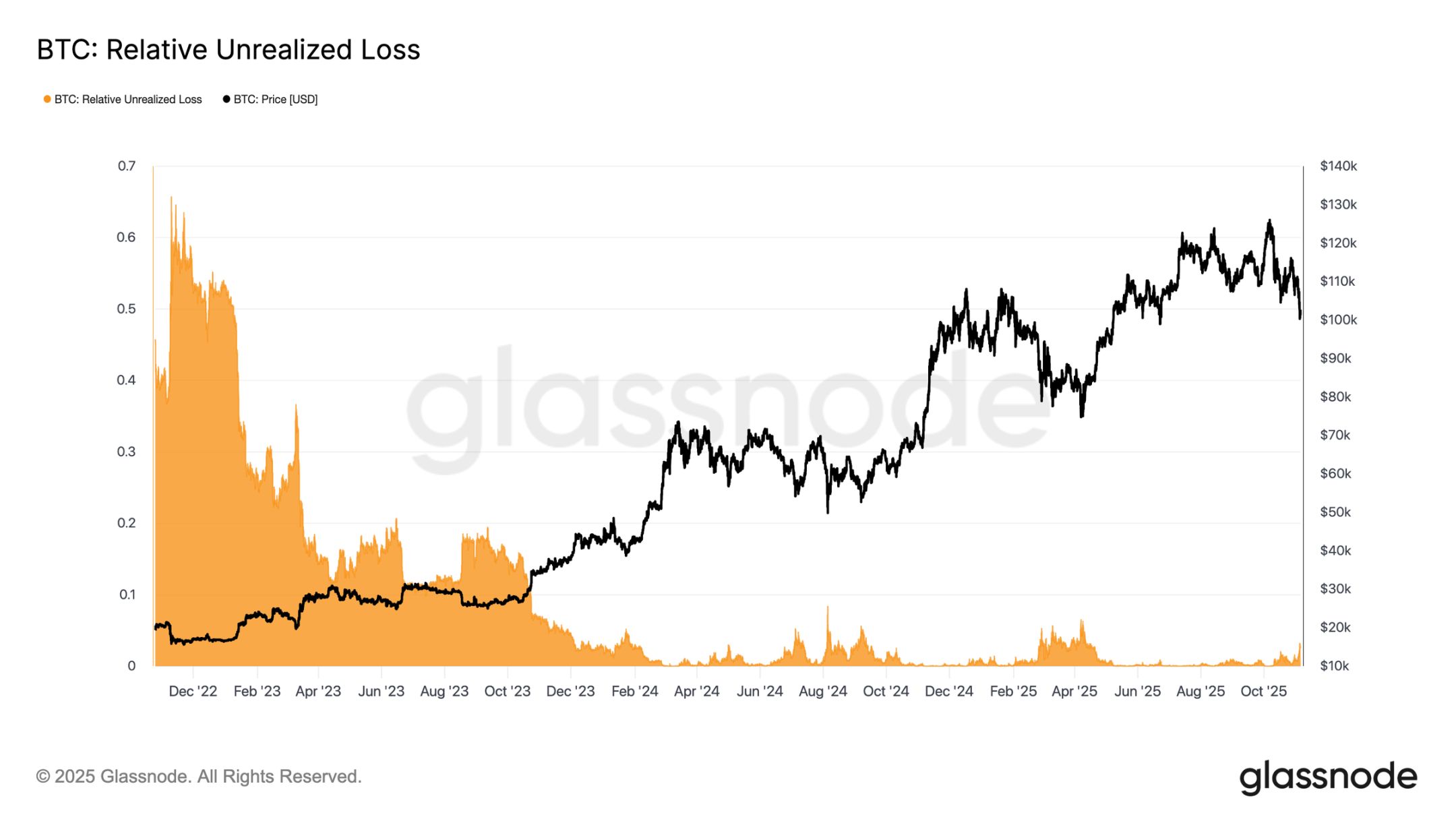

To further distinguish the nature of the current pullback, we can reference the relative unrealized loss rate—a metric that measures the proportion of total unrealized losses (in USD) to market cap. Unlike the extreme loss levels seen during the 2022–2023 bear market, the current 3.1% unrealized loss rate suggests mild market pressure, comparable to mid-term corrections in Q3–Q4 2024 and Q2 2025, and remains below the 5% threshold.

As long as the unrealized loss rate stays within this range, the market can be classified as a "mild bear market," characterized by orderly repricing rather than panic selling. However, if the pullback intensifies and this ratio exceeds 10%, widespread capitulation selling could be triggered, marking a shift to a more severe bear market structure.

Long-term Holders Continue to Sell

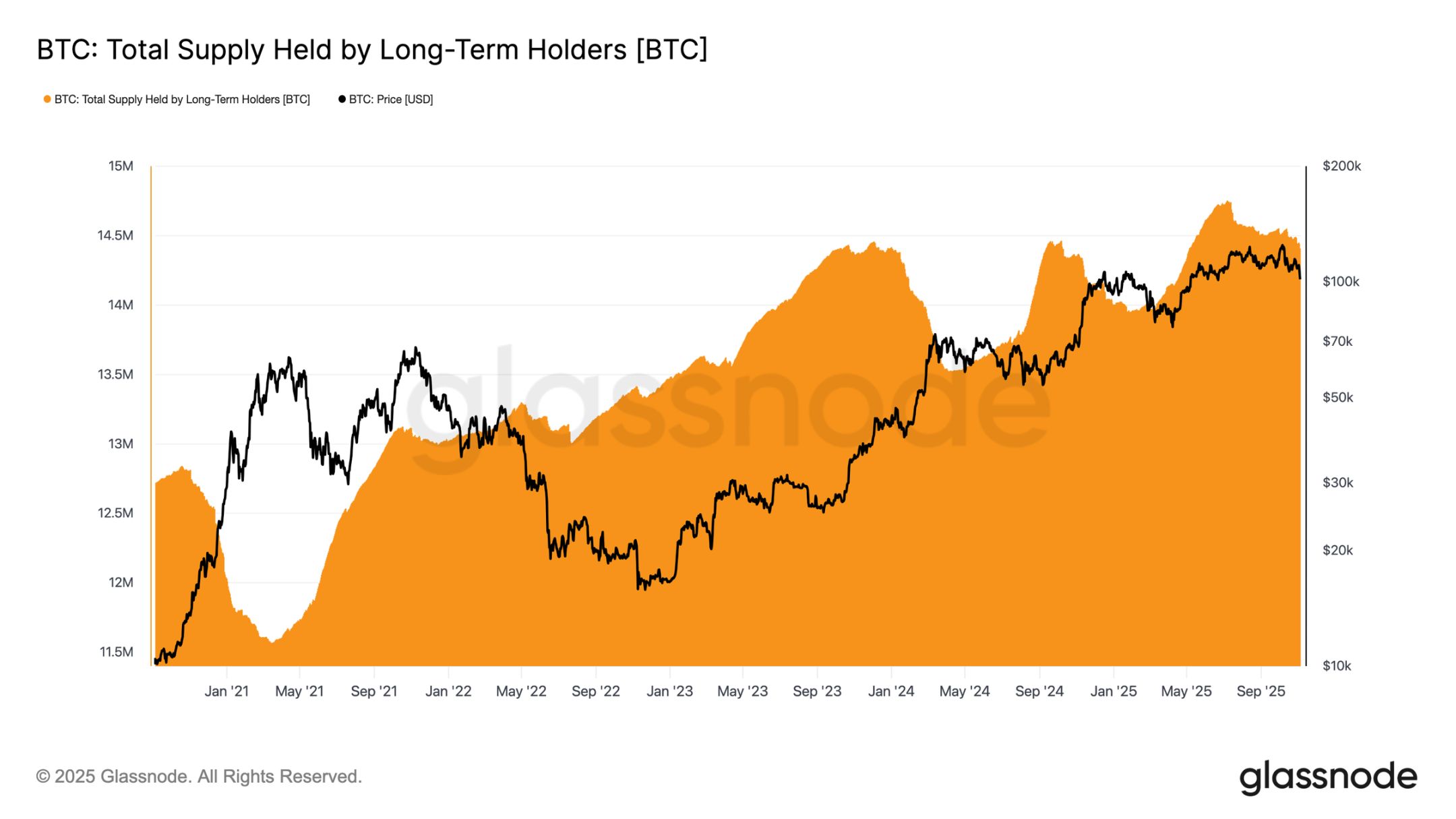

Despite losses being relatively manageable and only a 21% pullback from the $126,000 ATH, the market still faces mild but persistent selling pressure from long-term holders (LTH). This trend has gradually emerged since July 2025, and even Bitcoin’s new highs in early October did not reverse it, surprising many investors.

During this period, long-term holders’ Bitcoin holdings have decreased by about 300,000 coins (from 14.7 million to 14.4 million). Unlike the early cycle sell-off—when long-term holders "sold into strength" during sharp rallies—this time they are "selling into weakness," reducing holdings as prices consolidate and decline. This behavioral shift suggests experienced investors are showing deeper fatigue and waning confidence.

Off-chain Insights

Running Low on Ammunition: Institutional Demand Cools

Turning to institutional demand: Over the past two weeks, US spot Bitcoin ETF inflows have slowed significantly, with sustained net outflows of $150 million–$700 million per day. This stands in stark contrast to the strong inflows from September to early October, which provided price support at the time.

Recent trends indicate that institutional capital allocation has become more cautious, with profit-taking and a decline in new exposure dragging down overall ETF buying pressure. This cooling activity is closely tied to overall price weakness, highlighting a drop in buyer confidence after months of accumulation.

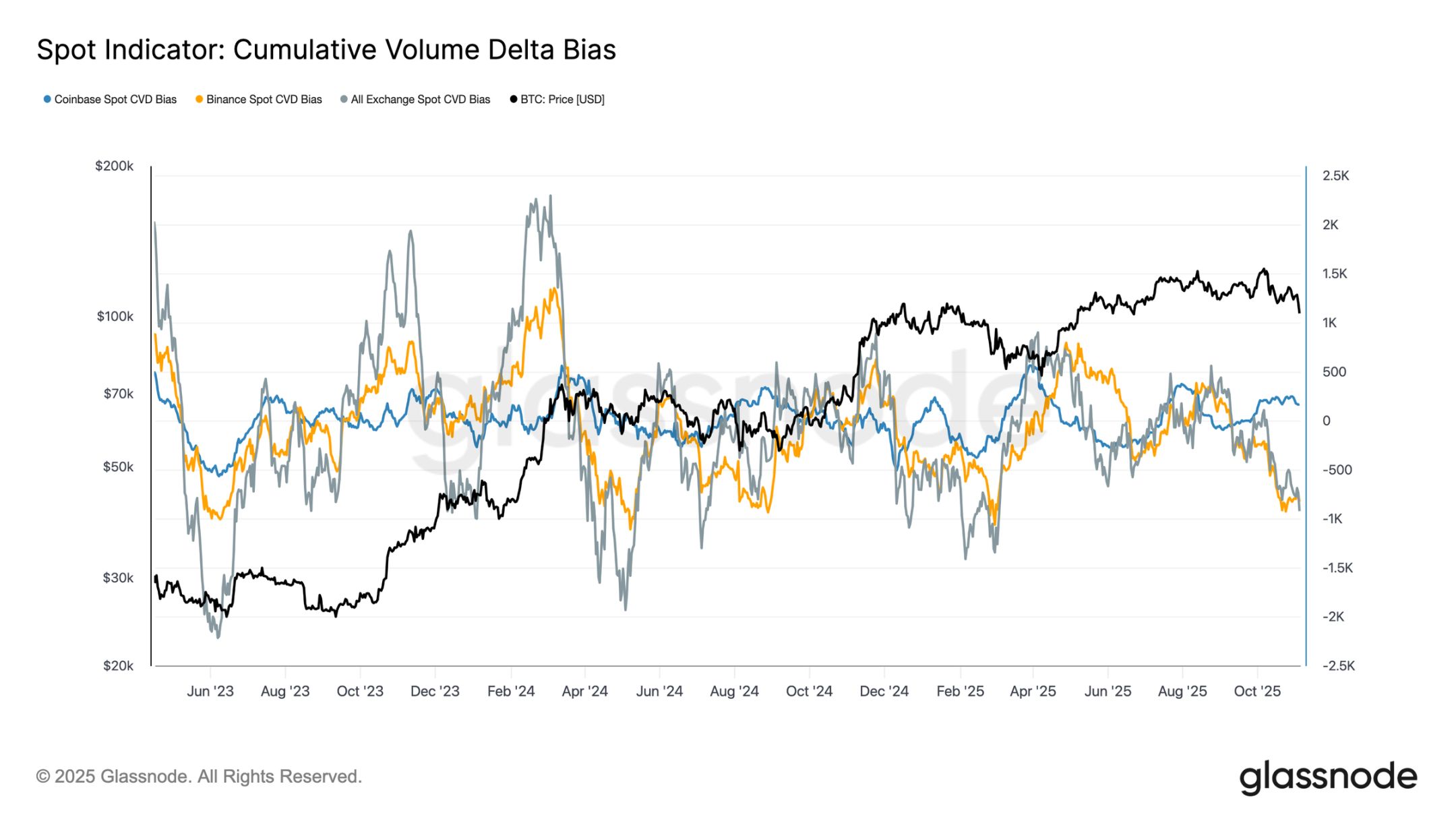

Clear Bias: Weak Spot Demand

Over the past month, spot market activity has continued to decline, with cumulative volume delta (CVD—a metric measuring the net difference between aggressive buying and selling) on major exchanges trending downward. Both Binance and overall spot CVD have turned negative, at -822 BTC and -917 BTC respectively, indicating persistent selling pressure and limited aggressive buying. Coinbase remains relatively neutral, with a CVD of +170 BTC, showing no clear signs of buyer absorption.

The deterioration in spot demand echoes the slowdown in ETF inflows, indicating a decline in self-directed investor confidence. These signals collectively reinforce the market’s cooling tone: buying interest is subdued and rebounds are quickly met with profit-taking.

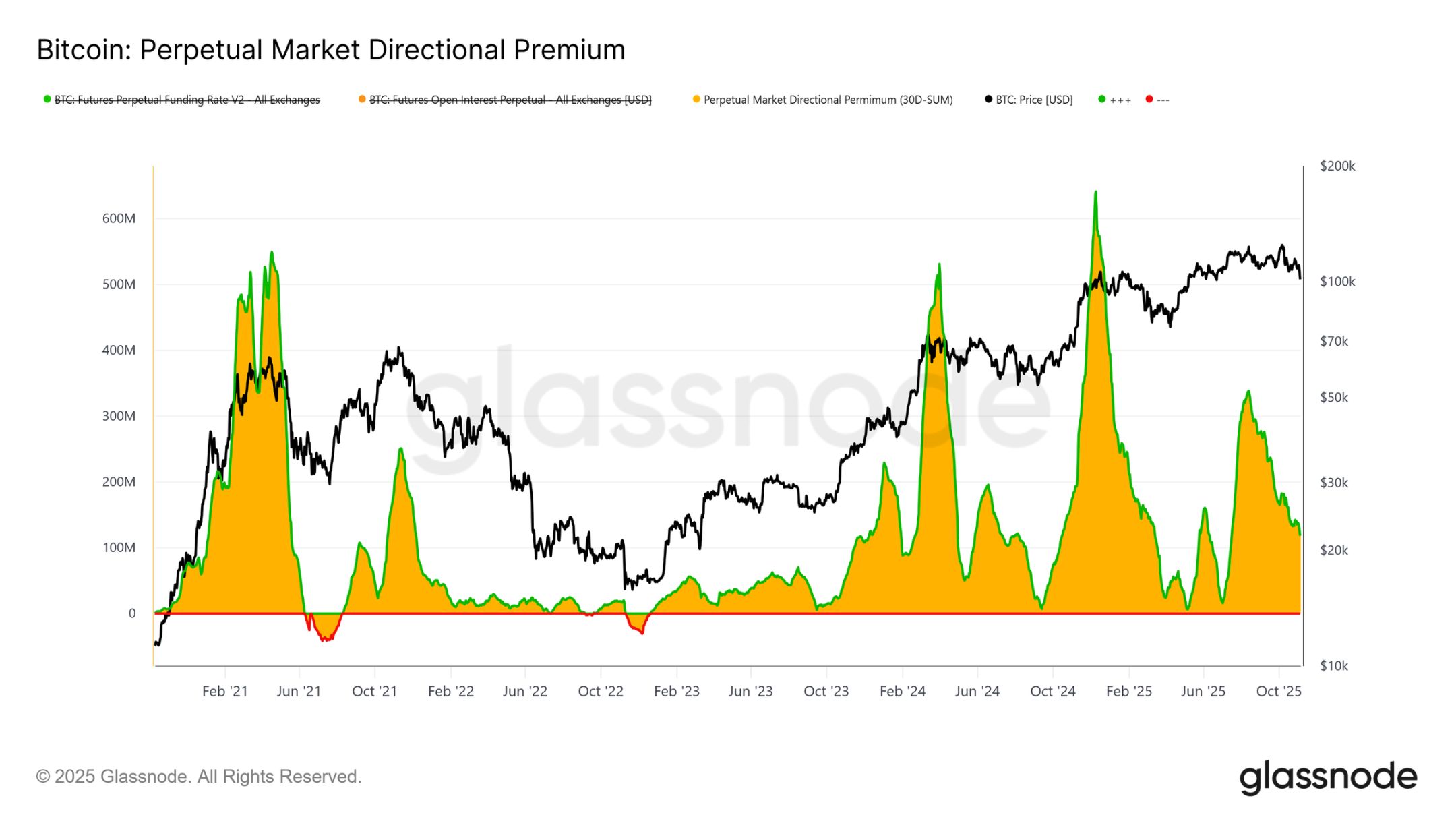

Interest Fades: Derivatives Market Deleveraging

In the derivatives market, the directional premium in perpetual futures (the fee paid by long traders to maintain positions) has dropped sharply from a peak of $338 million per month in April to about $118 million. This significant decline marks widespread closing of speculative positions and a clear cooling of risk appetite.

After a sustained period of high positive funding rates mid-year, the steady decline in this metric indicates traders are reducing directional leverage, leaning toward neutrality rather than aggressive long exposure. This shift aligns with the overall weakness in spot demand and ETF inflows, highlighting that the perpetual futures market has moved from optimism to a more cautious, risk-averse stance.

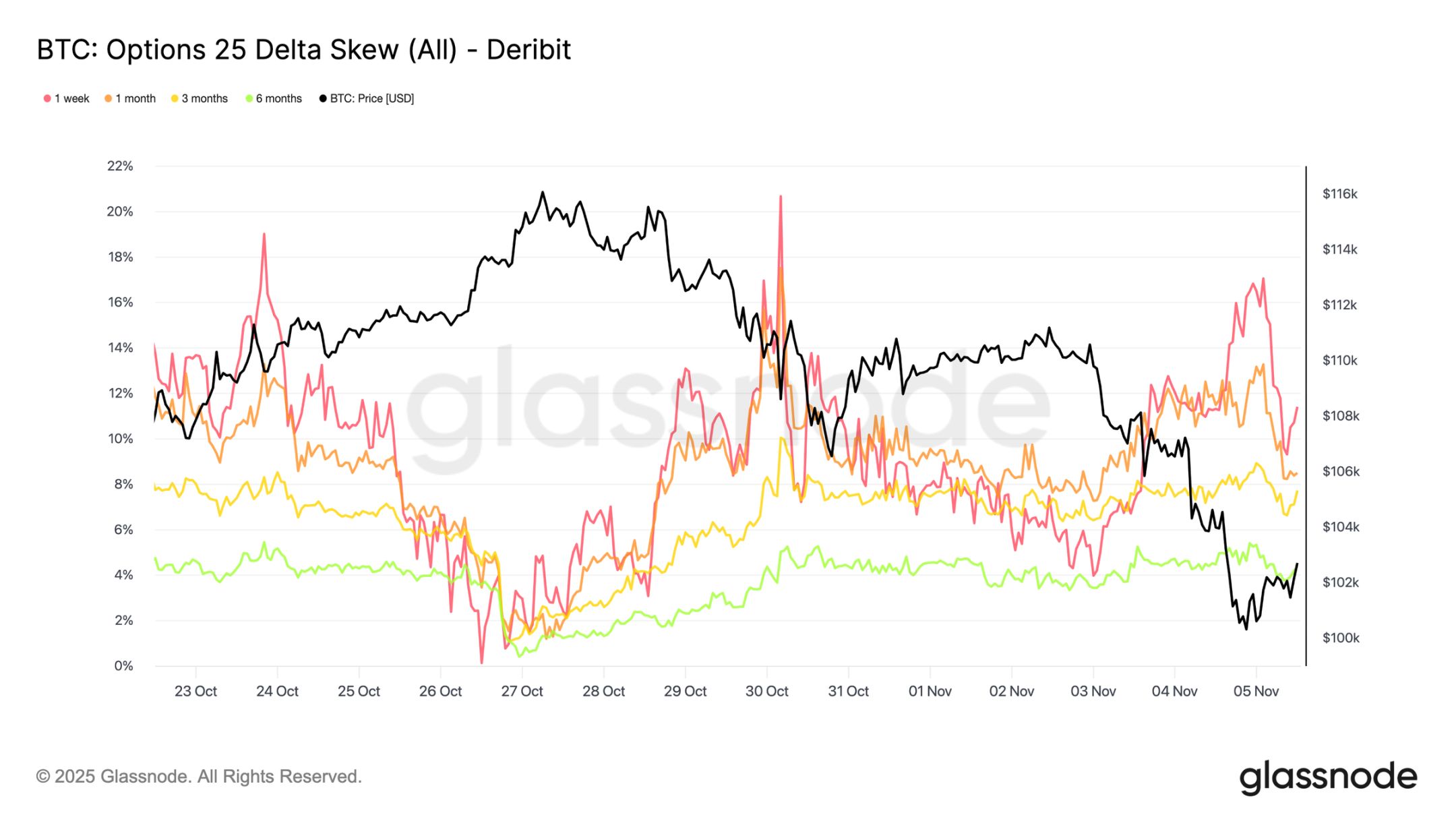

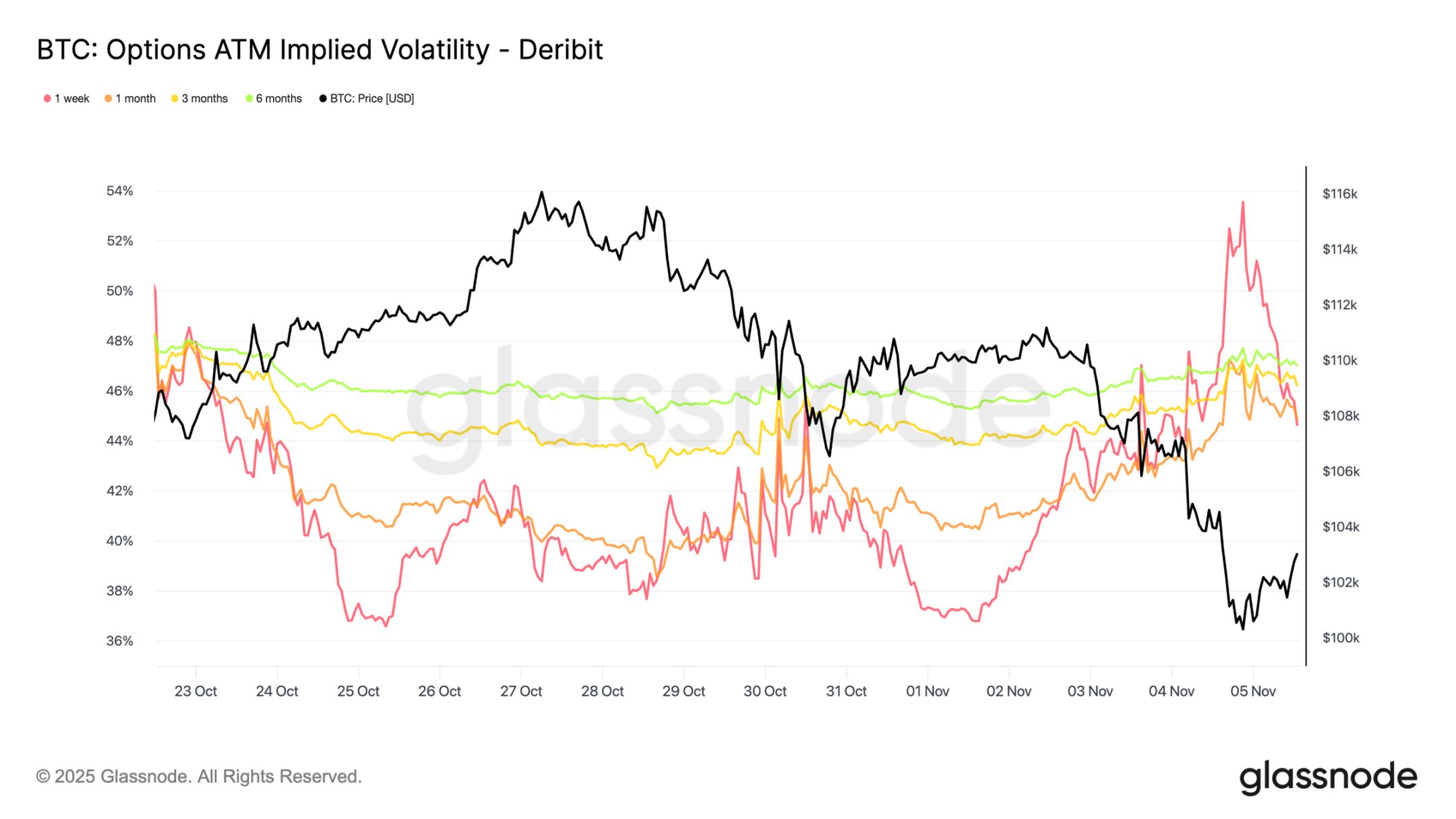

Seeking Protection: Defensive Tone in the Options Market

As Bitcoin hovers near the $100,000 psychological level, the options skew indicator unsurprisingly shows strong demand for put options. Data indicates that the options market is not betting on a reversal or "buying the dip," but is instead paying high premiums to guard against further downside risk. Put option prices at key support levels are elevated, showing traders remain focused on risk protection rather than accumulation. In short, the market is hedging, not bottom-fishing.

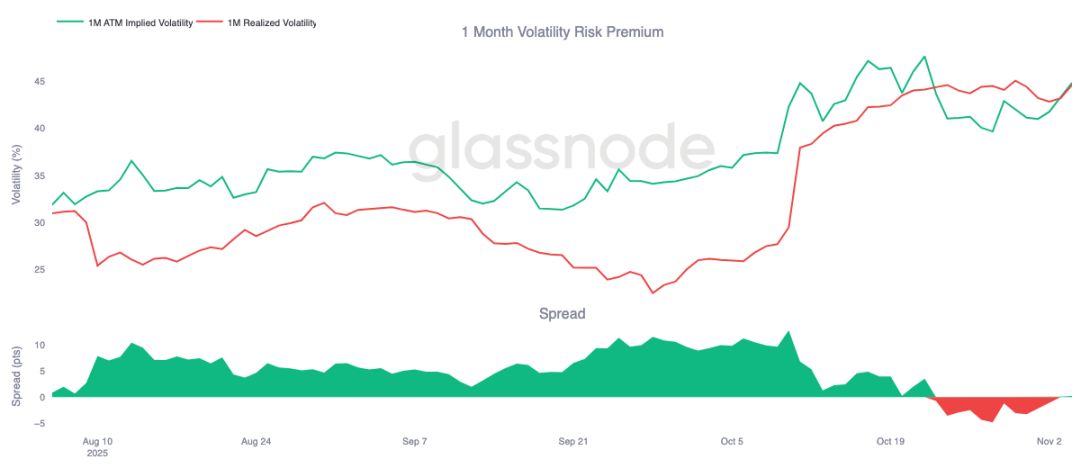

Risk Premium Rebounds

After ten consecutive days in negative territory, the one-month volatility risk premium has turned slightly positive. As expected, this premium has mean-reverted—after a tough period for gamma sellers, implied volatility has been repriced higher.

This shift reflects that the market remains dominated by caution. Traders are willing to pay high prices for protection, allowing market makers to take the other side. Notably, as Bitcoin fell to $100,000, implied volatility rose in tandem with the rebuilding of defensive positions.

Volatility Spikes and Retreats

Short-term implied volatility remains closely and inversely correlated with price action. During the Bitcoin sell-off, volatility spiked sharply, with one-week implied volatility reaching 54%, then falling back by about 10 volatility points after finding support near $100,000.

Longer-dated volatility also rose: one-month volatility increased by about 4 points from pre-correction levels near $110,000, and six-month volatility rose by about 1.5 points. This pattern highlights the classic "panic-volatility" relationship, where rapid price drops still drive short-term volatility spikes.

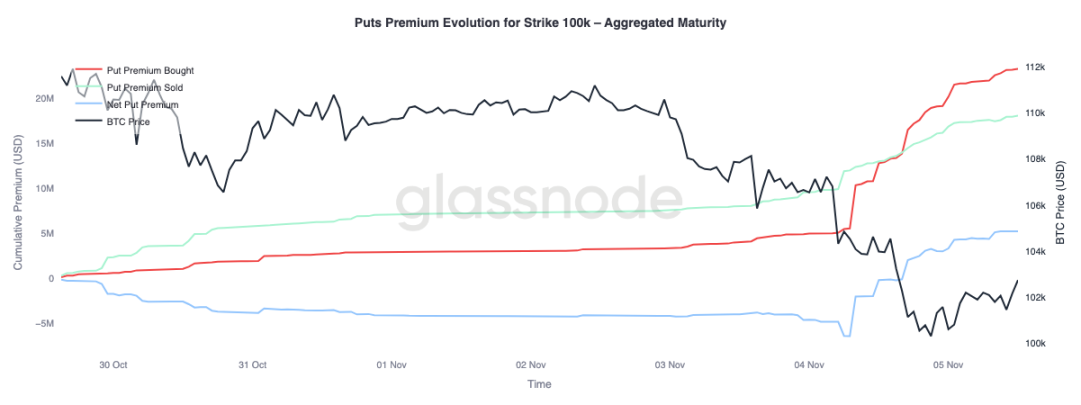

The Defensive Battle at $100,000

Observing the put option premium at the $100,000 strike provides further insight into current sentiment. Over the past two weeks, net put premiums have gradually risen, and yesterday, as concerns about the end of the bull market intensified, premiums spiked sharply. During the sell-off, put premiums surged, and even as Bitcoin stabilized near support, premiums remained high. This trend confirms ongoing hedging activity, with traders still choosing protection over renewed risk-taking.

Funds Flowing Defensively

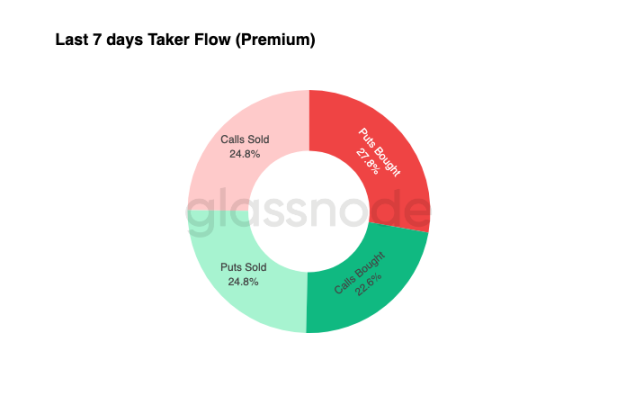

Fund flow data from the past seven days shows that aggressive trades are dominated by negative delta positions—mainly through buying puts and selling calls. In the past 24 hours, there is still no clear bottom signal. Market makers remain long gamma, absorbing significant risk from yield-seeking traders and potentially profiting from two-way price swings.

This setup keeps volatility high but manageable, and the market maintains a cautious tone. Overall, the current environment favors defense over aggressive risk-taking, lacking a clear upside catalyst. However, as downside protection remains expensive, some traders may soon start selling risk premium to seek value opportunities.

Conclusion

Bitcoin’s drop below the short-term holder cost basis (around $112,500) and stabilization near $100,000 marks a decisive structural shift in the market. So far, this correction resembles previous mid-term slowdowns: 71% (within the 70%-90% range) of supply remains in profit, and the relative unrealized loss rate is contained at 3.1% (below 5%), indicating a mild bear market rather than deep capitulation. However, the persistent selling by long-term holders since July and ETF outflows highlight weakening confidence among both retail and institutional investors.

If selling pressure persists, the realized price of active investors (around $88,500) will be a key downside reference; reclaiming the short-term holder cost basis would signal renewed demand strength. Meanwhile, both the directional premium in the perpetual futures market and CVD bias show a retreat in speculative leverage and declining spot participation, reinforcing a risk-averse environment.

In the options market, strong demand for puts, elevated $100,000 strike premiums, and a modest rebound in implied volatility all confirm a defensive tone. Traders continue to prioritize protection over accumulation, reflecting hesitation to call a "bottom."

Overall, the market is in a fragile balance: oversold but not panicked, cautious but structurally sound. The next directional move will depend on whether new demand can absorb the ongoing long-term holder selling and reclaim the $112,000–$113,000 range as solid support—or whether sellers will continue to dominate and extend the current downtrend.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Bitcoin’s valuation metric hints at a ‘possible bottom’ forming: Analysis

Bitcoin ‘$68K too low’ versus gold says JPMorgan as BTC, stocks dip again

$100B in old Bitcoin moved, raising ‘OG’ versus ‘trader’ debate

Bitcoin bulls retreat as spot BTC ETF outflows deepen and macro fears grow