Stablecoin yields are higher interest returns paid by crypto platforms on stablecoin deposits and are increasingly outcompeting bank savings rates. Stablecoin yields can reach ~5%, pressuring bank deposit margins and prompting calls for banks to raise rates or innovate to retain customers.

-

Stablecoin yields often exceed bank savings rates

-

Yield-bearing stablecoins can offer faster, lower-cost payments and no holding fees

-

Up to ~5% on some stablecoins vs. US average savings ~0.6% (Bankrate) — savers could gain materially

stablecoin yields: Compare yields vs bank savings and learn how banks can respond — read expert analysis and key takeaways.

What are stablecoin yields and how do they affect bank deposits?

Stablecoin yields are interest-like returns paid to holders who deposit stablecoins on crypto platforms. These yields can reduce traditional bank deposits by offering higher returns, pressuring bank profit margins and forcing banks to consider higher deposit rates or new products to retain customers.

How do stablecoin yields compare to bank savings rates?

Stablecoin yields on some platforms reach about 5%, while the US national average savings rate is roughly 0.6% and the best high-yield accounts are near 4% (Bankrate data). This gap makes yield-bearing stablecoins a competitive alternative for yield-seeking savers.

Why do experts say banks should raise rates instead of lobbying?

Industry voices, including Bitwise investment chief Matt Hougan, argue that banks should offer better deposit rewards rather than seeking regulatory limits on stablecoin yields. Hougan contends banks have historically benefited from low depositor returns and should compete by improving consumer rates.

When could stablecoins materially change local lending markets?

Smaller community banks that rely on retail deposits could see reduced deposits if large-scale adoption of yield-bearing stablecoins occurs. However, proponents say credit can migrate to decentralized finance (DeFi) channels where stablecoin holders supply liquidity directly, potentially offsetting local deposit losses.

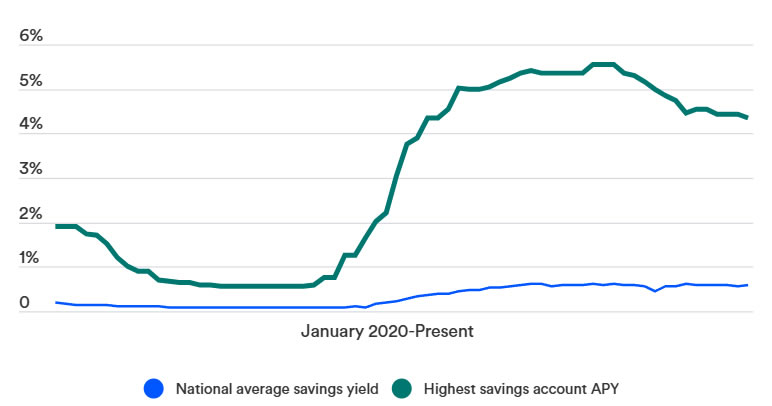

The highest-yielding US bank accounts offer a lower interest rate compared to most stablecoins. Source: Bankrate

The highest-yielding US bank accounts offer a lower interest rate compared to most stablecoins. Source: Bankrate

How should banks respond to stablecoin competition?

Banks can respond in several practical ways:

- Raise deposit rates to reduce the yield gap and retain customers.

- Develop competitive digital wallets and faster payment rails to match crypto convenience.

- Offer yield-bearing deposit alternatives structured to comply with regulations and protect consumer trust.

Frequently Asked Questions

Are yield-bearing stablecoins safe for retail savers?

Yield-bearing stablecoins carry risks including counterparty risk, platform solvency, and regulatory uncertainty. They can be higher-yielding but are not FDIC-insured, so savers trade deposit insurance for potentially higher returns. Assess platform credibility and terms before depositing.

Will stablecoins cause a bank run?

Experts disagree; while stablecoins can accelerate withdrawals, modern banks have wholesale funding options. Stablecoins could reduce bank deposits, but decentralized lending markets may absorb capital rather than causing systemic credit collapse.

Key Takeaways

- Yield gap: Stablecoin yields (~5%) exceed national savings averages (~0.6%), creating strong consumer incentives.

- Bank response: Raising deposit rates and improving digital services are pragmatic, market-based solutions.

- System impact: The main loser may be bank profit margins; the main winner could be individual savers seeking better returns.

Conclusion

Stablecoin yields are reshaping the competitive landscape for deposits, pushing banks to rethink rates and digital offerings. Policymakers and market participants must balance innovation, consumer protection, and financial stability as yields on stablecoins continue to attract depositors. Monitor official data and bank disclosures for ongoing developments.