IOSG: Why Has the Era of "Blindly Buying" Altcoin Seasons Become History?

The future altcoin market may tend towards a "barbell" structure, with one end comprising blue-chip DeFi and infrastructure, and the other end consisting of purely high-risk speculative tokens.

Original Title: "IOSG Weekly Brief|Some Thoughts on This Cycle's Altcoin Season #292"

Original Author: Jiawei, IOSG Venture

Introduction

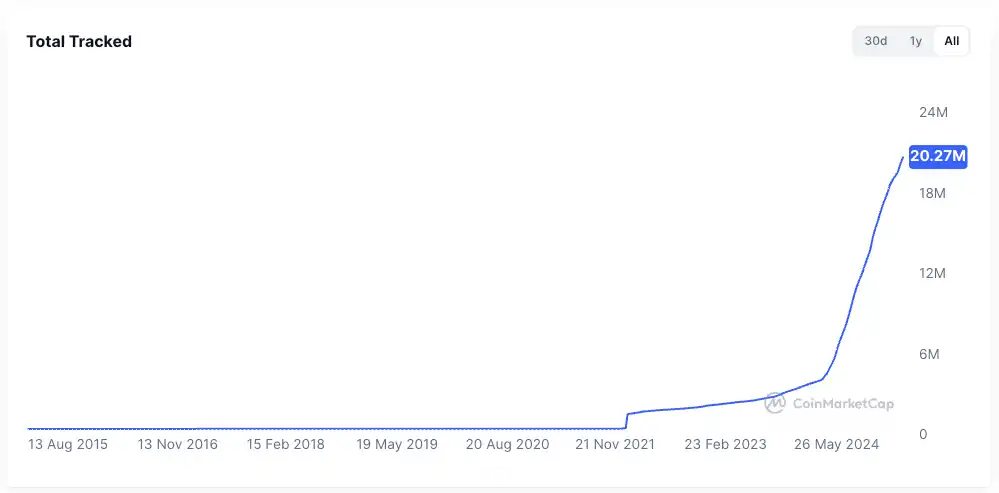

▲ Source: CMC

Over the past two years, the market's focus has always been drawn to one question: Will there be another altcoin season?

Compared to the strong performance and institutionalization of bitcoin, the vast majority of altcoins have performed poorly. Most existing altcoins have seen their market caps shrink by 95% compared to the last cycle, and even new coins with much hype are mired in difficulties. Ethereum also experienced a prolonged period of bearish sentiment, only recently recovering due to trading structures like the "coin-stock model."

Even with bitcoin hitting new highs and ethereum catching up and stabilizing, overall market sentiment towards altcoins remains sluggish. Every market participant is hoping for a repeat of the epic bull run of 2021.

I would like to put forward a core assertion: The kind of "flood-like" and months-long broad rally seen in 2021 is no longer possible due to changes in the macro environment and market structure. This does not mean that an altcoin season will never come, but rather that it is more likely to unfold in a slow bull pattern, with more pronounced differentiation.

The Fleeting 2021

▲ Source: rwa.xyz

The external market environment in 2021 was very unique. Amid the COVID-19 pandemic, central banks around the world were printing money at an unprecedented pace and injecting this cheap capital into the financial system, suppressing yields on traditional assets and leaving everyone with a sudden surplus of cash.

Driven by the search for high returns, capital began to flow massively into risk assets, with the crypto market becoming a major recipient. Most notably, the issuance of stablecoins expanded dramatically, soaring from about $20 billion at the end of 2020 to over $150 billion by the end of 2021—a more than sevenfold increase within the year.

Within the crypto industry, after DeFi Summer, on-chain financial infrastructure was being laid out, NFT and metaverse concepts entered the mainstream, and public chain and scaling tracks were in a growth phase. At the same time, the supply of projects and tokens was relatively limited, and attention was highly concentrated.

Take DeFi as an example: at that time, there were only a handful of blue-chip projects—Uniswap, Aave, Compound, Maker, etc.—that could represent the entire sector. Investors had fewer choices, making it easier for capital to work together and push the whole sector up.

The above two points provided fertile ground for the 2021 altcoin season.

Why "Good Times Don't Last, Grand Feasts Are Hard to Repeat"

Leaving aside macro factors, I believe the current market structure has undergone several significant changes compared to four years ago:

Rapid Expansion on the Token Supply Side

▲ Source: CMC

The wealth effect of 2021 attracted a large influx of capital. Over the past four years, the boom in venture capital has invisibly pushed up average project valuations. The prevalence of airdrop economics and the viral spread of memecoins have jointly led to a rapid acceleration in token issuance and rising valuations.

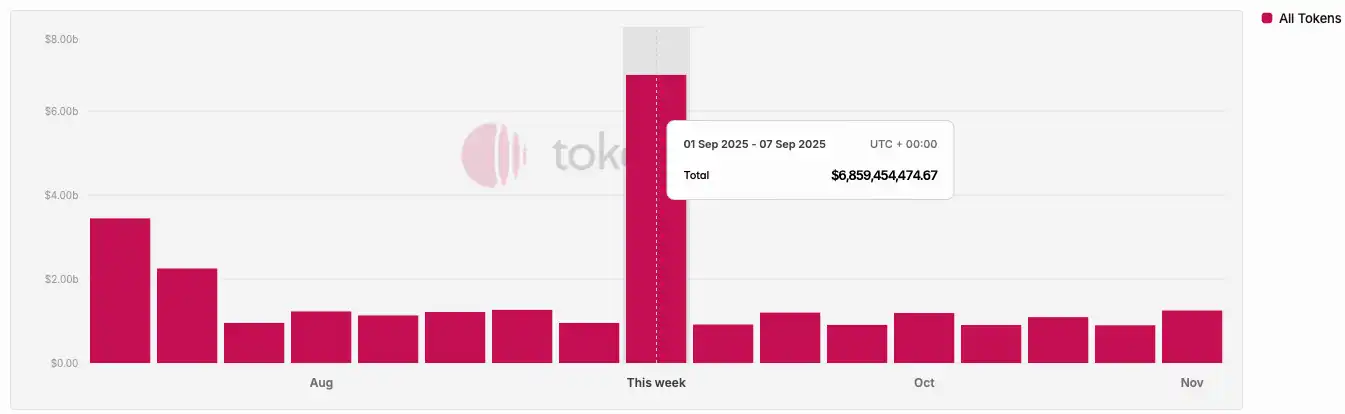

▲ Source: Tokenomist

Unlike in 2021, when most projects were in a high-circulation state, the current market—except for memecoins—sees mainstream projects generally facing huge token unlock pressures. According to TokenUnlocks, more than $200 billion worth of tokens are set to unlock in 2024-2025 alone. This is the much-criticized "high FDV, low circulation" industry status quo of this cycle.

Fragmentation of Attention and Liquidity

▲ Source: Kaito

In terms of attention, the chart above randomly samples the mindshare of Pre-TGE projects on Kaito. Among the top 20 projects, we can identify at least 10 different sub-sectors. If we were to summarize the main narratives of the 2021 market in a few words, most people would say "DeFi, NFT, GameFi/Metaverse." But in the past two years, it's hard to immediately describe the market with just a few words.

In this situation, capital switches rapidly between different tracks, with each cycle lasting only a short time. Crypto Twitter is flooded with overwhelming information, and different groups spend most of their time discussing different topics. This fragmentation of attention makes it hard for capital to form a unified force as it did in 2021. Even if a particular sector performs well, it rarely spreads to other areas, let alone drives a broad market rally.

On the liquidity side, a basic premise of altcoin season is the spillover effect of profitable capital: liquidity first flows into mainstream assets like bitcoin and ethereum, then seeks higher potential returns in altcoins. This spillover and rotation effect provides sustained buying support for long-tail assets.

This seemingly natural situation is something we haven't seen in this cycle:

· First, the institutions and ETFs driving bitcoin and ethereum's rise will not deploy their capital further into altcoins. These funds prefer custodial and compliant blue-chip assets and related products, which marginally strengthens the siphoning effect toward top assets, rather than raising the water level across the board.

· Second, most retail investors in the market may not even hold bitcoin or ethereum at all, but have been deeply trapped in altcoins over the past two years, leaving them with little spare liquidity.

Lack of Breakout Applications

The wild rally of 2021 was actually supported by some fundamentals. DeFi brought fresh liquidity to the long-stagnant blockchain application space; NFTs spread creator and celebrity effects outside the crypto circle, with growth coming from new users and new use cases (at least that was the story).

After four years of technological and product iteration, we find that infrastructure is overbuilt, but truly breakout applications are few and far between. Meanwhile, the market is maturing, becoming more pragmatic and clear-eyed—amid narrative fatigue, the market needs to see real user growth and sustainable business models.

Without a continuous influx of new blood to absorb the ever-expanding token supply, the market can only fall into a zero-sum game among existing participants, which cannot fundamentally provide the foundation needed for a broad rally.

Outlining and Envisioning This Cycle's Altcoin Season

Altcoin season will come, but it won't be like 2021's altcoin season.

First, the basic logic of profit rotation and sector rotation still exists. We can observe that after bitcoin reaches $100,000, its short-term upward momentum will obviously weaken, and capital will start looking for the next target. The same goes for ethereum afterward.

Second, in a market with long-term insufficient liquidity, altcoins held by investors are stuck, and capital needs to find ways to rescue itself. Ethereum is a good example: has ethereum's fundamentals changed this cycle? The hottest applications, Hyperliquid and pump.fun, did not happen on ethereum; the "world computer" narrative is also an old concept.

With insufficient internal liquidity, the only option is to look outward. Driven by DAT, and with ETH tripling in price, many stories about stablecoins and RWA have found a realistic foundation.

I envision the following scenarios:

Deterministic Rallies Driven by Fundamentals

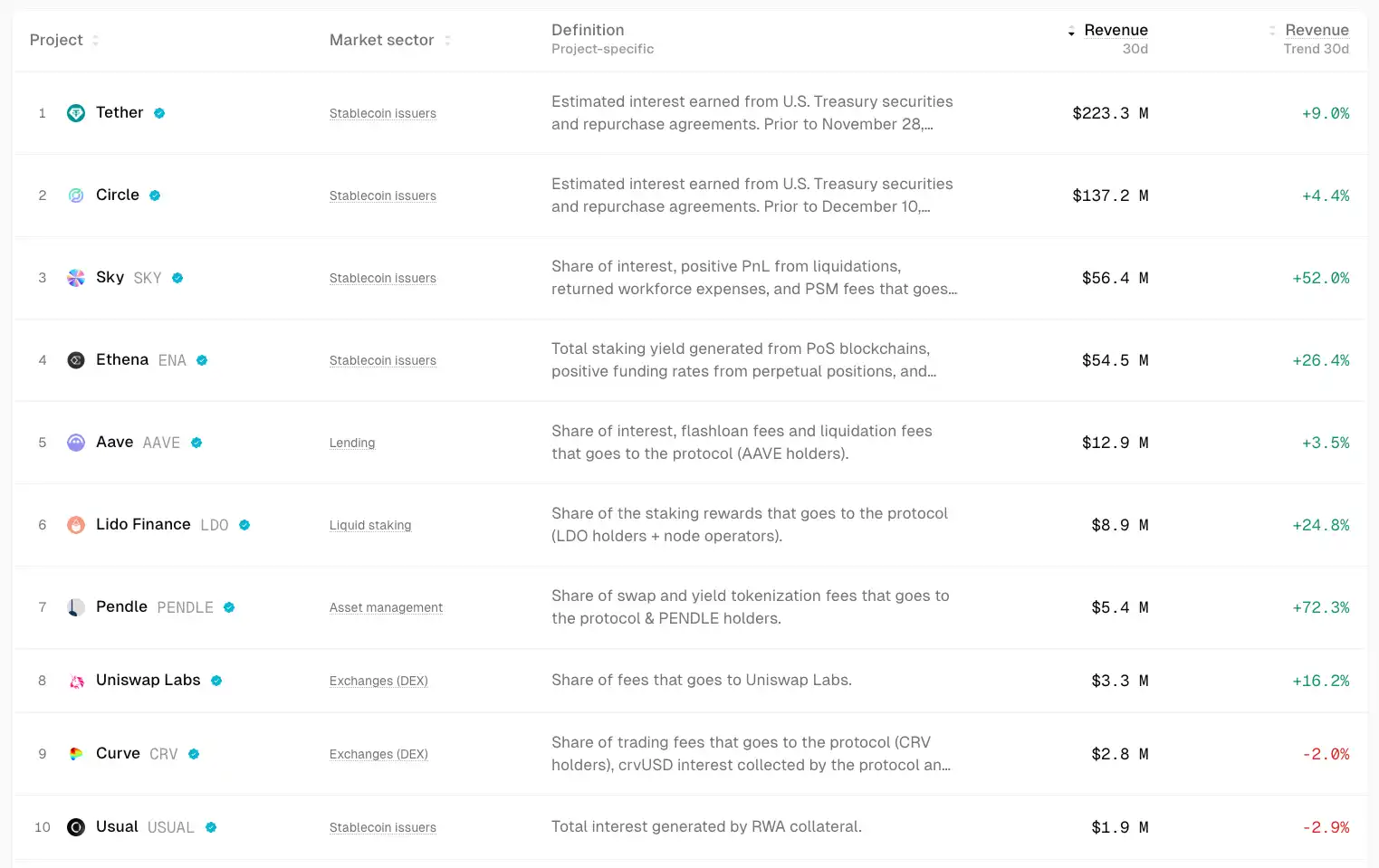

▲ Source: TokenTerminal

In an uncertain market, capital instinctively seeks certainty.

Funds will flow more toward projects with strong fundamentals and PMF. These assets may have limited upside, but are relatively more resilient and certain. For example, DeFi blue-chips like Uniswap and Aave have maintained good resilience even during market downturns; Ethena, Hyperliquid, and Pendle have emerged as new stars this cycle.

Potential catalysts could include actions at the governance level, such as turning on fee switches, etc.

The commonality among these projects is that they can generate considerable cash flow, and their products have been fully validated by the market.

Beta Opportunities in Strong Assets

When a main market line (such as ETH) starts to rise, capital that missed the rally or seeks higher leverage will look for highly correlated "proxy assets" to gain beta returns. Examples include UNI, ETHFI, ENS, etc. These can amplify ETH's volatility, but their sustainability is relatively weaker.

Repricing of Old Sectors Under Mainstream Adoption

From institutional bitcoin buying, ETFs, to the DAT model, the main narrative of this cycle is traditional finance adoption. If stablecoin growth accelerates—say, quadrupling to $1 trillion—these funds will likely partially flow into DeFi, driving a repricing of its value. Moving from crypto niche financial products into the traditional finance spotlight will reshape the valuation framework for DeFi blue-chips.

Localized Ecosystem Speculation

▲ Source: DeFiLlama

Due to its consistently high discussion heat, user stickiness, and aggregation of incremental capital, HyperEVM's ecosystem projects may experience several weeks to months of wealth effect and alpha during their growth cycle.

Valuation Divergence in Star Projects

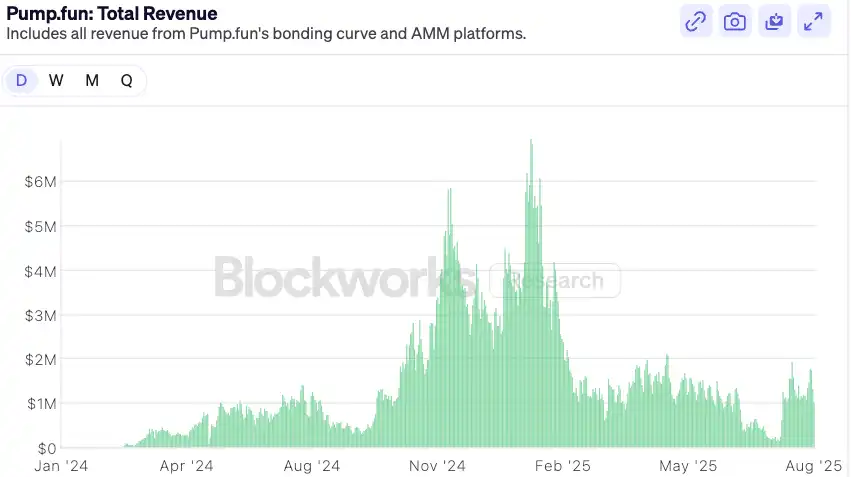

▲ Source: Blockworks

Take pump.fun as an example: after the emotional climax of its token launch fades and its valuation returns to a conservative range with market divergence, if its fundamentals remain strong, there may be a rebound opportunity. In the medium term, as the leader in the meme sector with income as fundamental support and a buyback model, pump.fun may outperform most top memes.

Conclusion

The "blind buy" altcoin season of 2021 is now history. The market environment is becoming relatively more mature and differentiated—the market is always right, and as investors, we can only keep adapting to these changes.

Based on the above, I also offer a few predictions as a conclusion:

1. After traditional financial institutions enter the crypto world, their capital allocation logic will be completely different from retail investors—they require explainable cash flows and comparable valuation models. This allocation logic directly benefits DeFi's expansion and growth in the next cycle. To compete for institutional capital, DeFi protocols will more actively initiate fee distribution, buybacks, or dividend designs in the next 6–12 months.

In the future, pure TVL-based valuation logic will shift toward cash flow distribution logic. We can see some recently launched DeFi institutional products, such as Aave's Horizon, which allows tokenized US Treasuries and institutional funds to be used as collateral for stablecoin lending.

As the macro interest rate environment becomes more complex and traditional finance's demand for on-chain yields increases, standardized, productized yield infrastructure will become highly sought after: interest rate derivatives (such as Pendle), structured product platforms (such as Ethena), and yield aggregators will benefit.

The risk DeFi protocols face is that traditional institutions, leveraging their brand, compliance, and distribution advantages, may issue their own regulated "walled garden" products to compete with existing DeFi. This is evident from the jointly launched Tempo blockchain by Paradigm and Stripe.

2. The future altcoin market may lean toward a "barbell" structure, with liquidity flowing to two extremes: on one end, blue-chip DeFi and infrastructure projects. These projects have cash flow, network effects, and institutional recognition, and will absorb most of the capital seeking steady appreciation. On the other end, purely high-risk speculative chips—memecoins and short-term narratives. These assets are not supported by any fundamental narrative, but serve as highly liquid, low-barrier speculative tools to meet the market's demand for extreme risk and return. Projects in the middle—with some products but insufficient moat or bland narratives—may find their market positioning awkward if the liquidity structure does not improve.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Crypto: The Fear Index Drops to 10, But Analysts See a Reversal

Uniswap Labs Faces Pushback as Aave Founder Highlights DAO Centralization Concerns

Ethereum Interop Roadmap: How to Unlock the “Last Mile” for Mass Adoption

From cross-chain to "interoperability," many of Ethereum's fundamental infrastructures are accelerating towards system integration for large-scale adoption.

A $170 million buyback and AI features still fail to hide the decline; Pump.fun is trapped in the Meme cycle

Facing a complex market environment and internal challenges, can this Meme flagship really make a comeback?