Why Fabrinet (FN) Just Got a Major Upgrade From JPMorgan: A Re-Rating in the Making Amid AI-Driven Demand

- JPMorgan upgrades Fabrinet to "Overweight" due to strong execution, scalability, and key AI infrastructure positioning. - The optical components sector faces supply-demand imbalances, but Fabrinet's expansion and high-growth clients (e.g., Nvidia) position it for $500M+ revenue by 2026. - Analysts highlight margin resilience and strategic diversification, though risks like supply constraints and tariffs remain. - The upgrade signals a re-rating opportunity as AI-driven demand accelerates, with Fabrinet l

The optical components sector is at a pivotal inflection point . As artificial intelligence reshapes global data infrastructure, companies like Fabrinet (NYSE: FN) are no longer just suppliers—they are architects of the next computing revolution. JPMorgan's recent upgrade of Fabrinet to “Overweight” from “Neutral,” coupled with a raised price target of $345 (a 17.33% upside), signals a shift in institutional sentiment. This move isn't merely about a stock rating; it's a vote of confidence in a sector grappling with supply constraints while racing to meet insatiable demand.

The Catalyst: Execution, Scalability, and Strategic Positioning

Fabrinet's Q4 performance was a masterclass in operational execution. The company delivered $2.65 in earnings per share, beating estimates by $0.02, and reported $909.69 million in revenue—a 20.8% year-over-year increase. These numbers aren't just impressive; they're indicative of a firm that has mastered the art of scaling in a fragmented industry. JPMorgan analyst Samik Chatterjee highlighted Fabrinet's exposure to “high-growth clients” like Nvidia , Ciena , and Amazon as a critical differentiator. Notably, the firm's potential role in Nvidia's 1.6T roadmap—a next-generation optical transceiver project—could generate up to $500 million in revenue by 2026. That's not just incremental growth; it's a structural tailwind.

The Bigger Picture: A Sector on the Brink of Re-Rating

The optical components industry is in the throes of a supply-demand imbalance. While AI-driven data center expansion and the adoption of co-packaged optics (CPO) are fueling demand, production bottlenecks persist. Fabrinet, which manufactures for hyperscalers and tech giants, has already flagged component shortages affecting 1.6T transceivers. Yet, this challenge is also an opportunity. The company is investing heavily in capacity expansion, including a new manufacturing facility, to address these constraints. JPMorgan's upgrade reflects the belief that Fabrinet can not only navigate these headwinds but emerge as a dominant player in a sector projected to grow at 30–35% annually through 2026.

Why This Upgrade Matters for Investors

JPMorgan's move aligns with broader analyst optimism. Ten analysts currently rate Fabrinet as a “Buy,” with a median price target of $349.50. The firm's rationale is twofold: first, Fabrinet's margin resilience—despite rising costs—demonstrates operational discipline; second, its expanding customer base and product portfolio position it to capture a larger share of the AI infrastructure boom. The stock's 40% year-to-date gain underscores its outperformance, but the upgrade suggests there's more to come.

However, investors must remain mindful of risks. Supply constraints could delay revenue realization, and geopolitical tensions—such as U.S. import tariffs—add volatility. Yet, Fabrinet's strategy to diversify manufacturing outside China and its focus on high-margin, proprietary technologies mitigate these concerns.

A Call to Action: Seizing the Re-Rating Opportunity

JPMorgan's upgrade isn't just a technical adjustment—it's a signal that Fabrinet is transitioning from a “neutral” bet to a “conviction” play. The stock's post-earnings pullback has created a compelling entry point for investors willing to bet on the long-term trajectory of AI infrastructure. With the optical components sector poised for sustained growth and Fabrinet demonstrating both scalability and innovation, this is a pivotal moment.

In a market where re-ratings are rare and fleeting, Fabrinet's story is one of the most compelling. For those who recognize the confluence of AI demand, supply constraints, and a company's ability to execute, the upgrade from JPMorgan is not just a green light—it's a siren call. The question isn't whether the sector will grow, but who will lead it. Fabrinet, it seems, is already ahead of the curve.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

‘Most hated bull run ever?’ 5 things to know in Bitcoin this week

Bitcoin price eyes $112K liquidity grab as US government shutdown nears end

This year's hottest cryptocurrency trade suddenly collapses—should investors cut their losses or buy the dip?

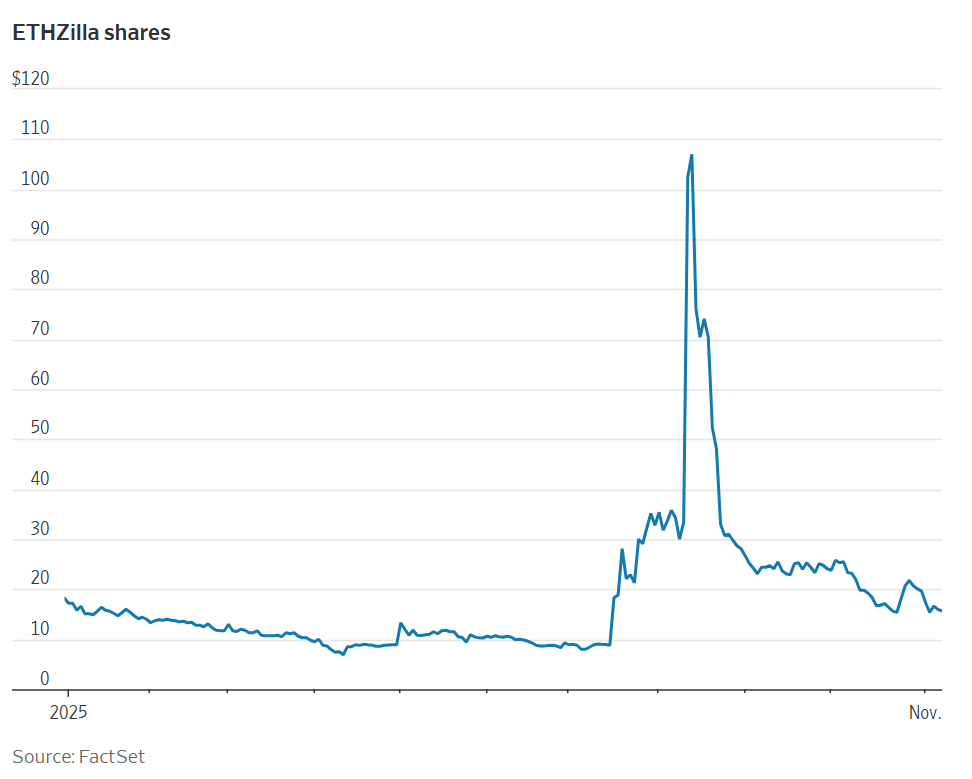

The cryptocurrency boom has cooled rapidly, and the leveraged nature of treasury stocks has amplified losses, causing the market value of the giant whale Strategy to nearly halve. Well-known short sellers have closed out their positions and exited, while some investors are buying the dip.

Showcasing portfolios, following top influencers, one-click copy trading: When investment communities become the new financial infrastructure

The platforms building this layer of infrastructure are creating a permanent market architecture tailored to the way retail investors operate.